A foreign address is a portfolio decision, not an exit

Indian millionaire numbers are rising while departures fall. Here's what the wealthy are actually doing

Consider two trends that are usually read as a contradiction.

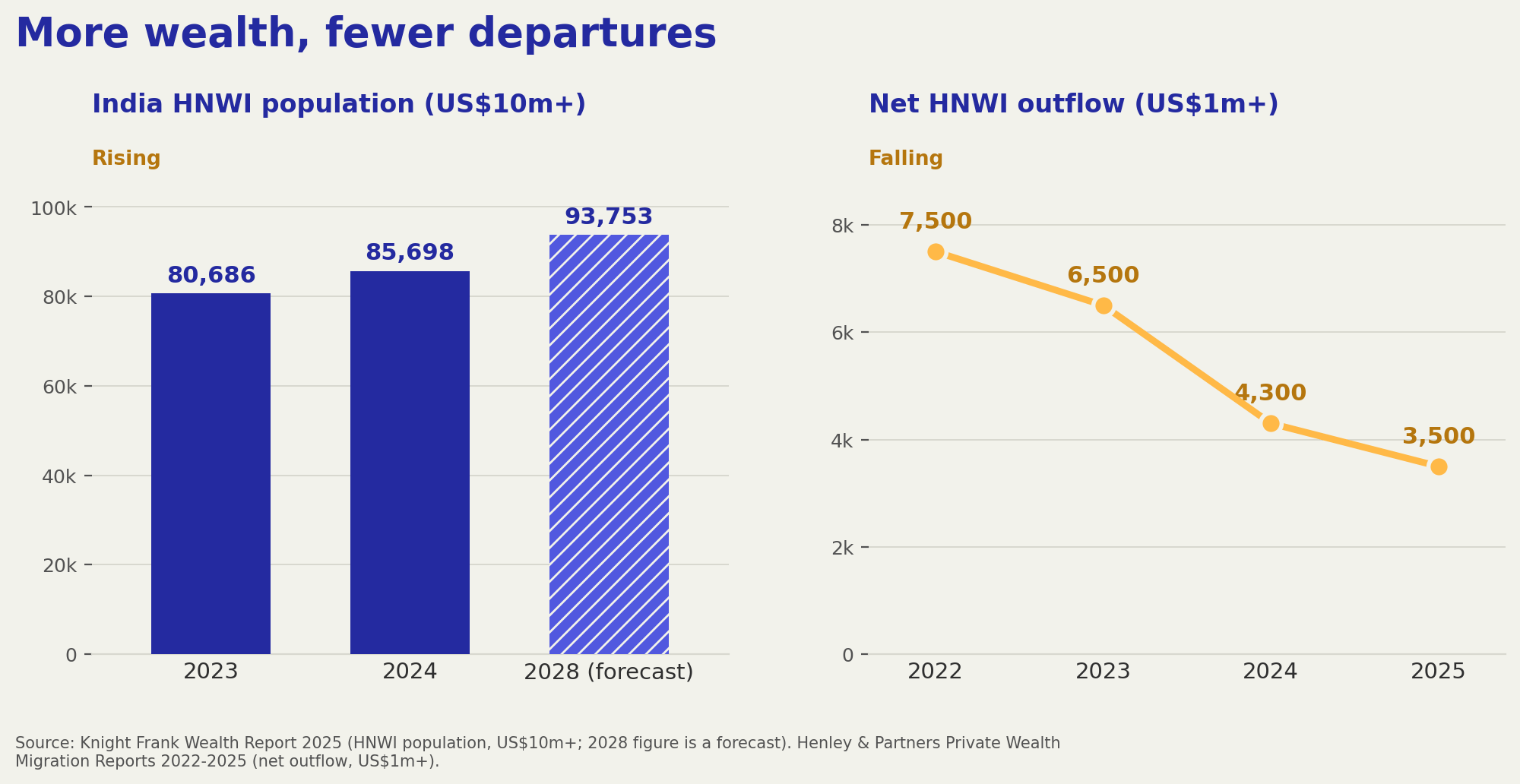

The first is the one that generates headlines. Henley & Partners, which has tracked private wealth migration for over a decade, has steadily lowered its estimate of net millionaire departures from India: a projected 7,500 in 2022, then 6,500, then 4,300, then roughly 3,500 for 2025. Read in isolation, that is a story about people leaving.

The second set of numbers tells you who is staying. Knight Frank’s Wealth Report 2025, which defines a high-net-worth individual as someone holding more than US$10 million in assets, puts India’s HNWI population at 85,698 in 2024, up 6% from 80,686 the year before, with a forecast of 93,753 by 2028. India now ranks fourth in the world for HNWI population, behind only the United States, China and Japan, and is home to 191 billionaires.

Hold the two together and the contradiction dissolves. The population of wealthy Indians is expanding, and the rate of departure is falling. Whatever is happening when an Indian family acquires a residence abroad, a mass exit is not it.

One point of fact matters before going further, because the language around this subject is often loose. India does not permit dual citizenship, so for most resident Indian families this is about acquiring residence rights abroad rather than a second passport, with citizenship typically a generational question that arises for children born or naturalised elsewhere.

With that established, the instinct to treat a foreign residence as a verdict on India misreads what these families are doing. They are not subtracting India from their lives. They are adding optionality around it. Henley’s own reporting supports this: the bulk of departing Indian millionaires retain their businesses and second homes in the country. The base stays. What changes is the number of doors the family can open.

This is the first myth worth retiring. A second base is not an exit. For most families who hold one, it is the opposite: a way of staying invested in India while no longer being wholly dependent on it.

What the wealthy are actually buying

If they are not buying an exit, what are they paying for?

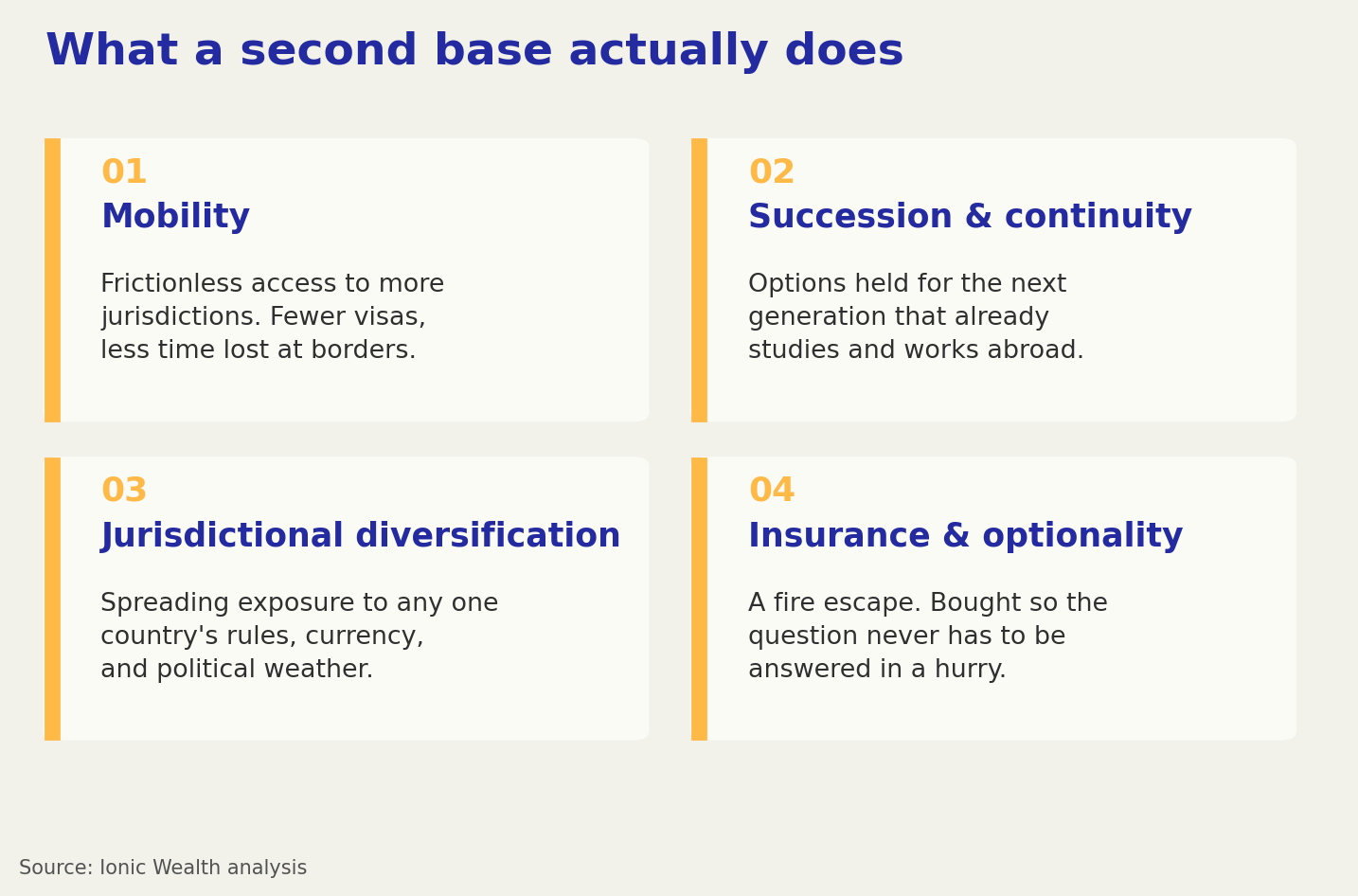

A second residence, or for the next generation an alternative citizenship, is an instrument, and like any instrument it has defined uses. This is the discipline the industry calls residence and citizenship planning, and stripped of both the romance and the alarm, it serves four functions.

The first is mobility. A travel document’s practical worth is measured by where it admits you without first asking permission. India’s passport has been climbing global rankings but still grants materially less frictionless access than the documents wealthy families increasingly want. For a household whose capital, businesses, and children already move across borders, visa friction is not an inconvenience. It is a recurring cost in time and certainty.

The second is succession and continuity. The capital that one generation built has to survive the handover to the next, and that next generation increasingly studies and works abroad. This is already visible in the money trail, not just the sentiment. Under the Reserve Bank of India’s Liberalised Remittance Scheme, outward remittances by resident Indians have grown from under US$10 billion a year half a decade ago to US$31.73 billion in FY24, before moderating to US$29.56 billion in FY25. Much of that flow goes to education and the maintenance of relatives overseas. A residence held by a child is simply the structural extension of a flow that is already happening.

The third is diversification of jurisdiction itself. An Indian UHNI family already diversifies across asset classes, currencies, and managers. The logic of not concentrating everything in one place does not stop at the portfolio. The 1986 Brinson, Hood and Beebower study in the Financial Analysts Journal taught a generation of investors that asset allocation, rather than security selection, drives most of the variation in long-term returns. The wealthiest families are now applying that same instinct one level higher, to the question of where the family itself is domiciled. A second jurisdiction spreads exposure to any single country’s rules, currency, and political weather.

The fourth is insurance. Most of what a second base protects against is a future the family hopes never arrives. It is the financial equivalent of a fire escape. You do not install one because you expect a fire. You install it so the question never has to be answered in a hurry.

Note what is absent from that list. None of the four functions requires leaving India, paying less tax in India, or thinking less of India. Each is about widening the family’s range of choices, not narrowing its commitments.

There is a useful regulatory signal here too. The framework that governs how Indian residents move money abroad has been loosening at the margin, not tightening. Budget 2025 raised the threshold above which tax is collected at source on LRS remittances from ₹7 lakh to ₹10 lakh. Budget 2026 went further on specific flows, cutting the TCS rate on remittances for education and medical purposes from 5% to 2%, effective 1 April 2026, while holding the ₹10 lakh threshold steady. The direction of regulations for cross-border planning is toward more room.

The mirror

There is a version of this conversation that treats a foreign passport or residence as a status object, the way an earlier generation treated an imported car. That version misreads it entirely.

The families who use these instruments well are not collecting passports. They are managing a single, unglamorous risk: that the one place where all of their capital, all of their family, and all of their future happens to sit could, at some point, become the wrong place to hold everything. That probability is low. It is also not zero. And for a family of sufficient means, the cost of insuring against it is modest relative to what is protected.

This is global investing for Indian investors at its most literal. Not an offshore fund or a foreign equity sleeve, but the family’s own footing, diversified.

Read correctly, the data is reassuring rather than alarming. The number of wealthy Indian families is rising. The number leaving is falling. And those who acquire a second base abroad are, for the most part, staying, building, and quietly buying themselves the option to be elsewhere if they ever need it.

A foreign address is not the exit. It is the part of the plan that ensures they never have to use it.

Very very neutral & unbiased conceptually with the purpose on concept of Second Home, with optionality of dual Citizendhip, on The Rising Bharat narrated 👌👌