Don’t write-off foreign RSUs, ESOPs in a falling market

Foreign RSU and ESOP holders get a smoother path to global equities than others.

Your new job’s offer letter just landed in your inbox. Along with a solid cash salary, the tech company has also offered RSUs of its US-headquartered parent company. Curious, you pull up the company’s stock chart, and the excitement quickly fades away. The company’s stock has fallen nearly 20% from its peak last year.

What seemed like a lucrative part of your compensation now begs the question: what are you supposed to do with it?

In a falling market, stock-based compensation, like Restricted Stock Units (RSUs) or Employee Stock Ownership Plan (ESOPs), may not feel worth it. However, to dismiss stock-based compensation when prices fall is no different from holding on to them blindly in a rising market, without evaluating what role they can play in your overall portfolio.

Over time, these RSUs and ESOPs have the potential to build into a significant portion of one’s wealth. In the case of foreign RSUs or ESOPs, they come with the added advantage of providing global diversification to one’s portfolio.

On the other hand, if the same employee wanted a direct exposure to these global stocks, it would come with additional costs and regulatory restrictions.

Global diversification

For employees receiving RSUs or ESOPs in a foreign-listed company, the exposure to global markets comes without the usual friction of investing abroad.

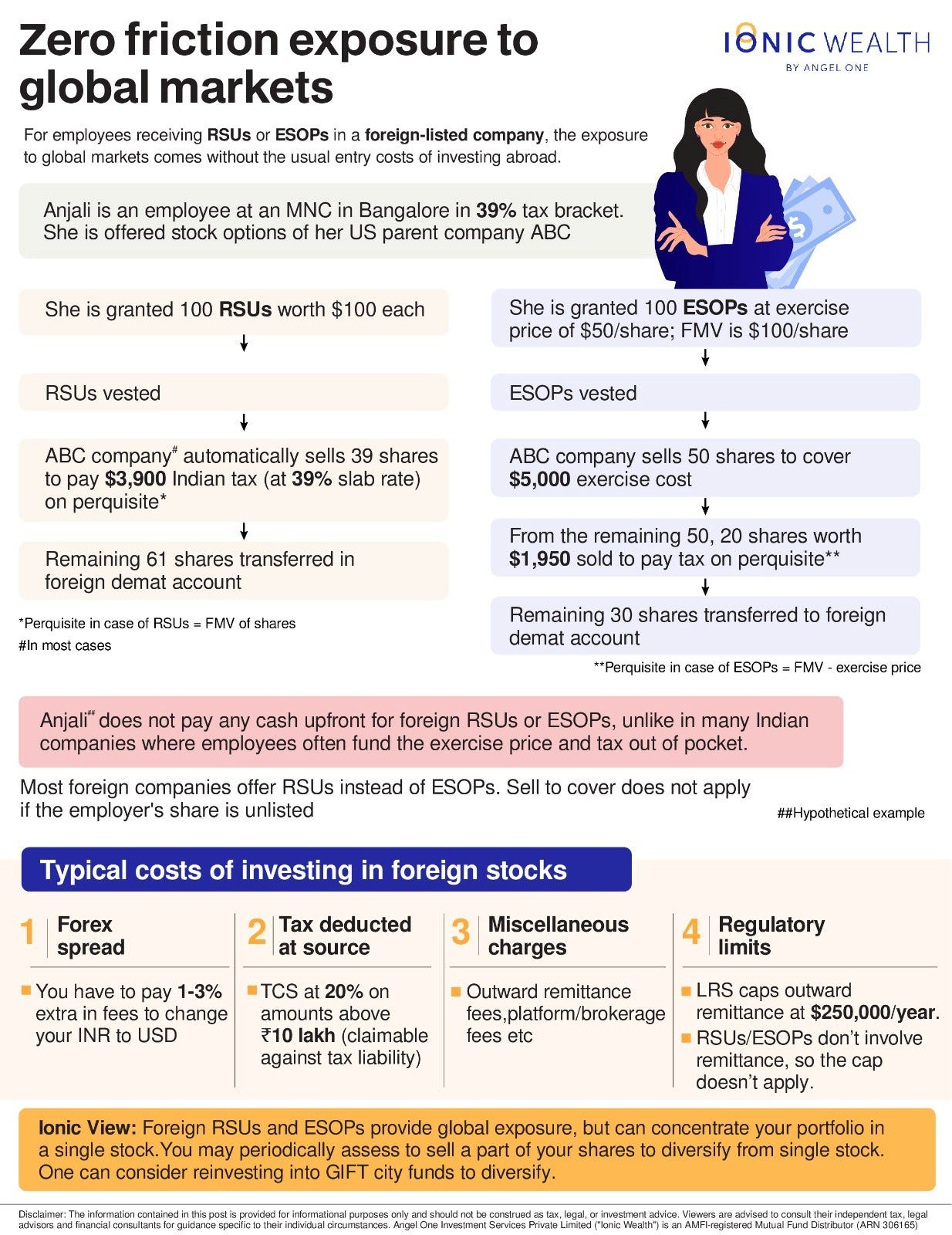

Take RSUs, for instance. When they vest, shares are transferred directly to the employee’s foreign demat account. There is no exercise price to pay, meaning the employee does not need to buy them using upfront cash. The fair market value (FMV) of the shares on the day of vesting is treated as a perquisite and taxed as salary income at the employee’s applicable income tax slab in India.

Say you are in the 39% tax bracket and have been granted 100 shares worth $100 each. In that case, $10,000 is treated as salary perquisite, and tax of $3,900 is payable in India.

Most of the employers will sell a portion of the vested shares to cover the Indian tax liability and the remaining shares are credited to your foreign brokerage account.

A similar sell-to-cover method is used for ESOPs too. Since ESOPs require the employee to pay an exercise price, a portion of the shares is sold to fund both the exercise cost and the tax liability.

In both cases, there is no separate outflow from your bank account to acquire these shares. Even after sell-to-cover reduces the number of shares you finally receive, you still benefit as you are acquiring the stocks at a discounted price than the FMV in the case of ESOPs, and no cost in the case of RSUs.

WATCH OUT: If the shares are unlisted, employees may need to pay tax and exercise price upfront.

Compare this with investing directly in US stocks. You need to remit money abroad under the LRS. Banks typically charge a forex spread of around 1-3% over the interbank rate. On top of that, there can be outward remittance charges. Once the money reaches the brokerage platform, you may pay a commission per trade or a flat platform fee to a foreign broker.

With stock grants, that friction doesn’t exist, and the exposure builds over time as grants vest.

Costs you incur when investing in foreign stocks on your own:

Forex spread of 1%–3%

TCS at 20% on amounts above ₹10 lakh (claimable against tax liability)

Miscellaneous charges: outward remittance fees, platform/brokerage fees etc.

When you receive foreign shares through RSUs or ESOPs, none of the above costs apply. And since no money is remitted outside India, your annual LRS limit of $250k is still available.

That said, stock options should not be mistaken for diversification in the pure sense. While the geography is different, the exposure is still concentrated in a single company.

Your salary and bonus already depend on the company’s business performance. On top of that, RSUs or ESOPs add another layer of exposure to the same stock. So a large part of your income and wealth is effectively tied to one company, and each vesting event increases that exposure.

Moreover, foreign stocks are generally USD or Euro denominated, and therefore, if the rupee weakens against these currencies, then you may be at an advantage.

One practical approach is to decide in advance how much exposure as a total percentage of your total global portfolio size or net worth you are comfortable with. Once that threshold is crossed, you can start trimming and diversifying systematically. Even partial selling at each vesting cycle can change the risk profile significantly over time.

How to approach your foreign RSUs and ESOPs

It’s crucial to understand the difference between how RSUs and ESOPs are structured.

RSUs are relatively straightforward. They are free-of-cost award stocks tied to a vesting schedule, usually spread over a few years. Vesting means the shares are released to you over time, based on conditions like continued employment, performance targets, promotions or other milestones. Once a tranche vests, the shares are directly transferred to your demat account and there is no buying price.

In listed companies, RSUs are effectively a guaranteed payout, as long as you stay through the vesting period.

Unlisted companies also offer RSUs. In such cases, while the shares are granted at a nil exercise price after the vesting period, employees cannot freely sell them. Liquidity is typically available only during specific events such as an IPO, buyback, or secondary sale.

Whether you are offered ESOPs or RSUs, it is important to read the fine print, as it can materially affect what you finally get.

Another clause to watch is whether vesting is back-loaded across multiple years, meaning a smaller portion vests early and a larger portion vests later. This structure is designed to improve retention, because leaving early can mean losing a large part of the grant.

Also pay attention to clauses that define what happens to your stock options during events such as acquisitions, demergers, resignation or termination.

For professionals receiving RSUs or ESOPs in foreign-listed companies, the arrangement offers a meaningful structural edge over peers trying to build global exposure on their own.

Together, these three advantages make foreign stock-based compensation far more than a line item in an offer letter. When managed thoughtfully, it can become one of the most efficient wealth-building tools available to the salaried professional.

With inputs from Hardik Mehta, Lead-tax at Ionic Wealth

Disclaimer: The information contained in this post is provided for informational purposes only and should not be construed as tax, legal, or investment advice. Viewers are advised to consult their independent tax, legal advisors and financial consultants for guidance specific to their individual circumstances. Angel One Investment Services Private Limited ("Ionic Wealth") is an AMFI-registered Mutual Fund Distributor (ARN 306165)